As of January 1st, 2025, certain large companies and groups will be required to publish and certify information on sustainability issues, in accordance with Directive No. 2022/2464 of December 14, 2022, known as the CSRD (Corporate Sustainability Reporting Directive), transposed by Ordinance No. 2023-1142 of December 6, 2023, clarified by Decree No. 2023-1394 of December 30, 2023.”

The relevant information must allow for an understanding of “the company’s impact on sustainability issues, as well as how these issues affect its business development, results, and financial position.” This information will include environmental, social, and governance aspects, and must appear in a specific report on sustainability issues which will be part of the management report (except for non-EU companies which will have to make a distinct report).

The new obligation to consult with the SEC will be introduced in this context.

Purpose of the new SEC Consultation

In the companies concerned, the SEC must be consulted on information relating to sustainability issues, on the means of obtaining and verifying this information, and within the framework of the three existing recurrent consultations: strategic orientations, economic and financial situation, and social policy (new version of Article L. 2312-17 of the Labor Code).

It is important to note that the law does not introduce a new specific and distinct consultation but integrates sustainability into the existing consultations.

The companies concerned must, therefore, prepare for this obligation by adapting their internal consultation processes on the three annual themes and, where necessary, informing / training SEC members.

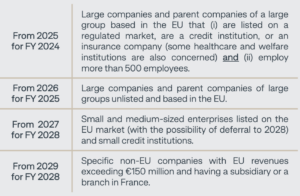

Companies in scope and deadlines

The companies affected by the new consultation obligation are those having a SEC in France and required to establish a sustainability reporting (or exempt from this obligation as another employee of the group is subject to the obligation).

The scope of this obligation will progressively extend according to the following simplified calendar:

Large, small and medium-sized companies, as defined in Article L. 230-1 of the Commercial Code, and large groups defined in Article L. 230-2 of the same code, are those that meet financial and headcount thresholds specified by Decree. An information notice from the Finance Ministry details the companies and groups concerned.

Monitoring compliance with the SEC consultation

The statutory auditor, or an independent third-party body, will have to verify the compliance of the sustainability information published by companies and ensure that the SEC consultation on this information has been integrated within the three recurring consultations.

In the event of non-compliance, the auditor or independent third-party body must report it in their certification report and alert the governing bodies and, if necessary, the AMF (Financial Markets Authority). Any criminal offense noted may be reported to the Public Prosecutor.

In this respect, the absence of certification of the information and the hindrance to this certification are heavily sanctioned criminal offenses.

This monitoring is aimed at enhancing the transparency and credibility of the information provided in the specific report on sustainability issues included in the management report, as well as ensuring the involvement of employee representatives on this matter.